Equity markets recovered strongly in April and volatility declined significantly from peak panic levels in March. Major equity benchmarks closed the months roughly 30% off bear-market lows which were reached on March 23rd.

Main drivers for the rally were the substantial fiscal and monetary stimulus packages put in place by governments and central banks around the globe – most notably in the US. The Federal Reserve’s actions contributed to a sharp fall in investment grade and high yield spreads and kept Treasury yields low, despite the rising budget deficit and sovereign debt levels.

The COVID-19 pandemic has infected well over three million people— more than 1 million in the U.S. alone—and claimed the lives of nearly 250,000 globally.

In April, new infections have started to decrease and Western countries are slowly re-opening their economies while the extent of lasting damage to the real economy is not yet clear.

Despite first signs of medical progress, the crisis is still far from over. Although the introduced stimulus measures are already enormous, more may still be needed.

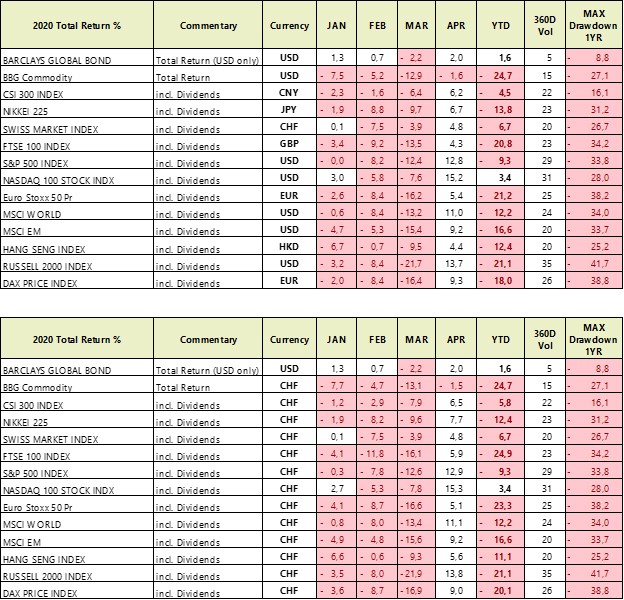

- In April, developed stock markets outperformed those of emerging countries.

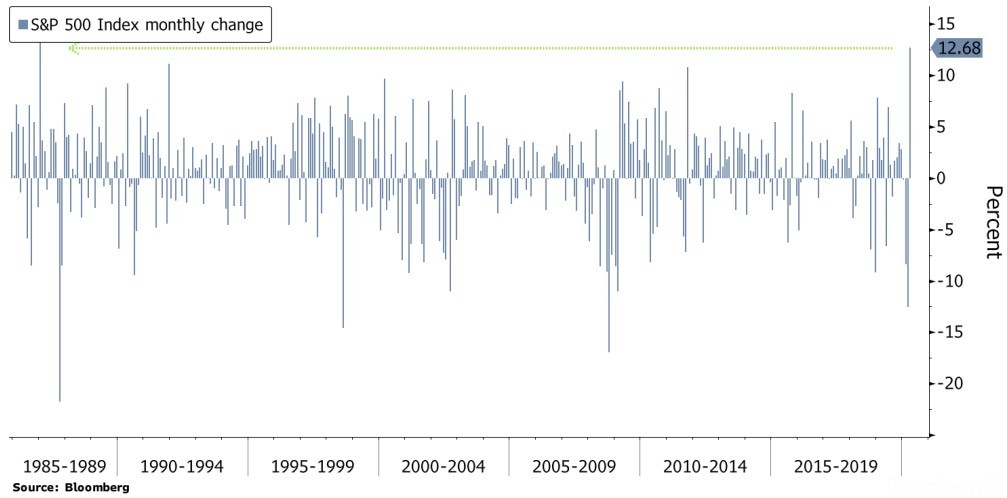

- The S&P 500 index generated a total return of +12.82% (price return of +12.68%) in April and recovered almost 60% of its previous decline.

- <

- The monthly rally for the S&P 500 marks its best since 1987, and the best April since 1938.

The Nasdaq Composite’s rise (total return +15.2%) was its best since 2000, and its best April on record. >

>

- Companies sold about USD 300 billion of US investment-grade bonds in April, the greatest volume for any month on record. Another sign that the Federal Reserve so far has been successful in calming credit markets.

- In commodity markets, WTI Oil prices dropped into negative territory as the monthly futures rollover panicked the market in light of shrinking storage capacity.

- If refineries don’t want oil and if there is virtually no more storage (or the fear of storage running out), oil can become a liability and have negative value.

- The US real GDP contracted at an annualized rate of 4.8% in the first quarter.

- The number of applications for unemployment benefits rose by 30 million in the last six weeks.

- The extent of the economic deterioration due to the shutdown was also evident in April’s Flash Composite Purchasing Managers’ Index (PMI) which fell to 27.4.

- The Federal Reserve committed itself to unlimited purchases of government bonds and will now also buy corporate high yield bonds, provided the issuer had an investment grade rating before March 22nd.

- Euro-zone real GDP contracted by 3.8% in the first quarter.

- The April composite Flash PMI indicator for the euro zone fell to an all-time low of 13.5, confirming a substantial economic decline.

- The European Central Bank continued its program of quantitative easing and applied a degree of flexibility by placing greater emphasis on buying government bonds of those countries which had the greatest need due to the virus, such as Italy and Spain.

- While the Western world was going through peak viral growth numbers, China’s economy has been gradually reopened.

- In the first quarter, China’s real GDP declined by 6.8% year-on-year. The urban unemployment rate fell to 5.9% in March from 6.2% in February.

- Overall, there has been a recovery in production, retail sales and investment in April.

Brief Market Commentary:

- Despite April’s market rebound and the unprecedented policy response, considerable uncertainty remains over the trajectory of global growth and financial markets over the coming quarters.

- A lot will depend on the extent to which economies can successfully reopen, and whether the US weighing retaliatory actions against China over the coronavirus will turn out to be more than pre-election rhetoric.

- We believe patience, caution and selectivity in investment selection remain key.

Sources: Bloomberg, JPM, Barclays, Citigroup, Morgan Stanley, Dow Jones Market Data, Goldman Sachs

Total Returns YTD as of April 30th 2020: