Market View

The Fed, AI and a Bruised but Intact Bull Market

created by Ullrich Fischer, Chief Investment Officer

-

Shock, Resilience, and Resolution: Na...Market View April 2026

-

Geopolitics Increase Volatility – Fun...Market View March 2026

-

Markets, Volatility & Productivit...Market View February 2026

-

Goldilocks First, Overheating Later —...Market View January 2026

-

Dovish Fed Pivot, Labor Softening &am...Market View December 2025

-

The AI Supercycle, Fed Easing & a...Market View November 2025

-

Skepticism Fuels the Bull: Under-Owne...Market View October 2025

-

AI Momentum, Fed Shift, Inflation WatchMarket View September 2025

-

Rally Faces Headwinds: Markets Remain...Market View August 2025

-

The return of Goldilocks is taking shapeMarket View July 2025

-

Resilient stock markets have more roo...Market View June 2025

-

Markets Recover Despite Fragile Senti...Market View May 2025

-

US Tariffs and Their Impact: Risks fo...Market View April 2025

-

Market Upheaval: US Protectionism and...Market View March 2025

-

Markets on the move: Volatility, AI c...Market View February 2025

-

After the Rally: Market Volatility an...Market View January 2025

-

Positive momentum and US exceptionali...Market View December 2024

-

Resilient US growth amid election unc...Market View November 2024

Executive Summary

The events of the first half of 2026 have shaken the bull market, but in our view they have not derailed it. The US economy is accelerating and already showing early signs of overheating, while oil is once again moving more normally through the Strait of Hormuz, easing both energy prices and geopolitical tension. Yet the Iran war has ended the Goldilocks backdrop of steady growth and disinflation, and the debasement trade (the preference for real assets such as gold) has come under pressure.

On monetary policy, the defining event of the quarter was Kevin Warsh’s first meeting as Chair of the Federal Reserve. We saw it primarily as an attempt to rebuild central-bank credibility. Warsh sought to refocus policy on the Fed’s inflation mandate and began dismantling forward guidance – the practice of signaling to markets the Fed’s most likely next move. As we read it, his strategy is to sound tough now, earn market credibility and buy time for inflation to cool as energy prices mean-revert, ultimately avoiding a hiking cycle.

We judge this bull market against three tests: it must not be a bubble, the economy must avoid recession, and Fed policy must remain supportive. The first two still pass comfortably: earnings are booming and growth is reaccelerating. Only the third is in question. The risk we respect most is a policy error: a Warsh-led Fed skipping the wait-and-see phase and moving straight to rate hikes, echoing Powell’s 2018 mistake of overtightening at the start of his Fed tenure.

We therefore remain constructive but are prepared for a choppier few months: taking some profits while continuing to lean into the structural winners and actively managing the risks created by market concentration. Through it all, inflation data remains the single most important indicator to watch.

Market Review – Second Quarter 2026

It was the strongest quarter for US equities since 2020, with the market adding roughly USD 8 trillion in value. The rally was global too: the MSCI All-Country World Index recorded its best quarter since late 2020.

Yet beneath the headline strength, market leadership remained narrow. Semiconductor makers and the broader AI trade drove most of the gains, rebounding sharply from war-driven lows and delivering their strongest six-month performance relative to the S&P 500 on record. Although they account for less than one-fifth of the index, they have generated roughly 70% of its year-to-date advance of +10.2% total return in USD. At the same time, the AI trade has fractured: investors continue to reward the infrastructure suppliers building the boom, while scrutinizing the cloud platforms (a significant part of the “Mag 7”) that are paying for it.

Momentum was the winning factor. The factor, which captures the continued outperformance of stocks already rising the fastest, is now beating the broader S&P 500 by the widest margin since the late 1990s.

The Bull Market’s Three Pillars

We view this bull market as resting on three pillars. The first is that we do not see an equity bubble ready to burst; prices are being driven by profits rather than hope. On that test, the market passes. Forward earnings estimates for the S&P 500 have risen 18% this year, the second-fastest first-half increase on record. Analysts now expect roughly 23% profit growth for 2026 as a whole – only the seventh time in three decades that earnings have grown by 20% or more. That kind of surge is usually seen coming out of a recession, not years into an expansion.

Source: Goldman Sachs Global Investment Research

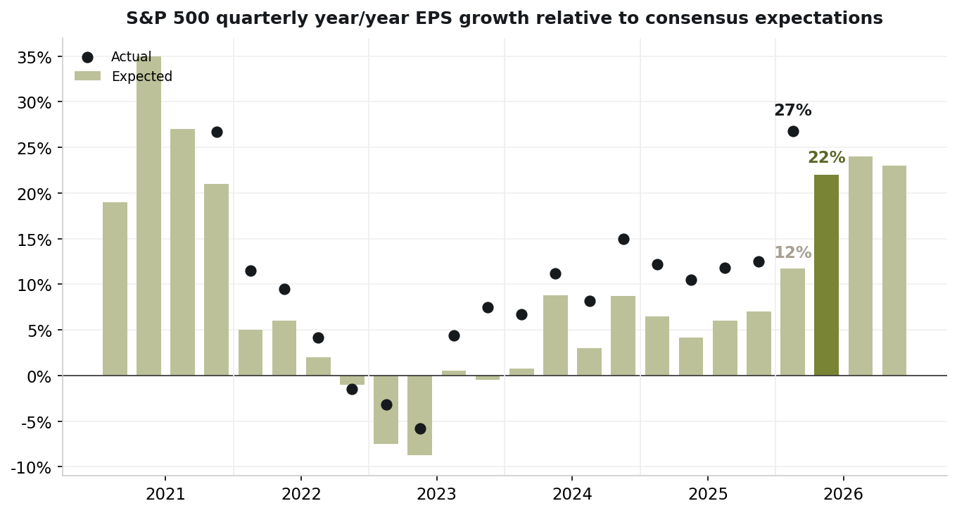

Companies beat expectations: first-quarter earnings grew by about 27%, well above the 12% initially expected. Analysts now expect 22% in the second quarter, the highest bar going into a reporting season since 2021.

Valuations are not extreme either: the Magnificent Seven mega-caps trade at about 24 times expected earnings, only a modest premium to the wider market.

Some bubble concerns focus on falling AI token costs as a sign of weakening demand. In our view, the more important signal – GPU availability through cloud providers – points in the opposite direction: the chips that power AI remain scarce, especially Nvidia’s newest Blackwell processors. Demand at the core of the AI cycle is still running hot.

The reopening of the market for new listings is another sign of vitality. After the record SpaceX debut, OpenAI and Anthropic are preparing to go public, likely in the next 12 months, with a combined value that could exceed USD 2 trillion. Nor is the activity limited to IPOs: to fund the AI buildout, the mega-caps are raising capital on a remarkable scale. Alphabet alone launched a USD 80 billion stock sale, alongside a wave of big-tech bond issuance that topped USD 120 billion last year. The market has absorbed all this remarkably well, with deals heavily oversubscribed.

The second pillar is that the economy avoids recession. Far from slowing, the US and other developed economies are, in our view, reaccelerating. The AI buildout is a key reason here too: spending by the largest cloud companies has reached roughly 2.5% of US GDP, providing a tailwind to the broader economy as long as it continues. Even with some cracks in housing and hiring, an imminent recession looks unlikely. Once the capex cycle turns, this will weigh on growth; for now, we see no sign of that.

The third pillar, supportive Fed policy, is now the one in question – and the source of the main risk. The cautionary tale is 2018: likewise a US midterm year, with Trump in office, similarly strong earnings growth and Powell in his first year as Fed chair. Keen to establish hawkish credentials, Powell said in October 2018 that rates were “a long way from neutral,” kept raising them, and by December the S&P 500 was down almost 20%. He then had to U-turn into easing mode. If Warsh were to repeat that playbook, the third pillar would crack. That is not our base case, but it is the risk we take most seriously for the second half of the year.

The Fed – A New Start at a Delicate Juncture

We think Warsh is trying to rebuild the Fed’s credibility at a delicate moment. The economy is stronger than many expected, and inflation has been above the 2% target for five years. The backdrop has shifted quickly: in January, markets expected a rate cut by December; Iran-war-driven inflation and a firmer jobs market have since flipped that to one or two rate hikes priced by year-end.

Yet much of the inflation fight the Fed might want has already been delivered by markets: oil is back near pre-war levels, real yields (the yield left after market-implied inflation) have risen, and financial conditions have tightened. The clearest evidence is in inflation breakeven rates – the inflation rate markets expect, inferred from the gap between ordinary and inflation-protected US government bonds.

Source: Bloomberg

Expected inflation one year ahead has collapsed from a March peak above 5% to around 1.4% now, while five- and ten-year expectations remained anchored throughout the Hormuz crisis and have recently moved closer to 2%.

In other words, markets are signaling a sharp near-term drop in inflation and no lasting problem. That is precisely where an overly hawkish Fed – perhaps too anchored in the memory of having once been too soft on post-pandemic inflation – risks tightening too much, too quickly.

History offers a humbling reminder as well: as the chart below shows, almost every new Fed chair gets tested, with a median first-year equity-market drawdown of about 17%. Most new Fed chairs initially lean hawkish until the market pushes back. Whether Warsh can avoid that pattern remains the open question.

Source: Strategas

We view Warsh first and foremost as a political figure. At his first FOMC meeting, his message appeared calibrated to speak to both sides of the inflation debate and, in part, to reassure committee members who believe the Fed must assert its independence from President Trump. He took a similar approach this week at the ECB Forum in Sintra.

A few of Warsh’s comments in Sintra stood out. For example, he acknowledged falling inflation expectations, a point he had ignored just two weeks earlier.

“Inflation risks have come down in the last four weeks.”

“If you wanted me to sound like a pessimist and a doomer on this [AI], I’m afraid I’m not there.”

“…we were trying to suppress volatility. That was the right policy for a crisis. It is not the right policy in the time that we have now.”

His actions so far, including the creation of five task forces to review key Fed issues, suggest to us that he may be doing little more than buying time.

“My hope, my aspiration, is that nine to 12 months from now we’re going to be using new technologies to understand what’s happening in the real economy in a contemporaneous, real-time way that positions us as central bankers to make better decisions.”

In our view, Warsh will ultimately not engineer a hawkish long-term reset; fiscal realities leave him little room to do so. We thus expect the Fed to keep rates steady this year. There is no 2022-style wage-price spiral, and the intellectual core of the FOMC continues to signal an extended pause, not a hike. We also expect the task forces to lean dovish overall, although their findings are unlikely to arrive before year-end. In the meantime, policy risk remains elevated.

Gold – Tactical Headwinds, Strategic Strength

We have long held a strong overweight in gold, one of our best-performing positions of the past decade. After a powerful multi-year rally, and with the near-term backdrop becoming less favorable, we are trimming our overweight. This is a risk-management step, not a reversal of our long-term conviction.

The immediate headwinds are real yields, which have risen sharply as the Fed has leaned more hawkish, lifting the opportunity cost of holding gold. Together with a firm dollar and fading speculative flows, this has pushed gold into its worst quarter in more than a decade. We see the selloff more as capitulation by short-term traders than as a broken thesis. That said, from a technical perspective gold needs to reclaim roughly USD 4,400 an ounce before the tactical setup becomes more constructive.

The long-term case remains firmly intact in our view. Fiscal fragility in developed markets is stark: US federal debt held by the public has reached about 100% of GDP, while the fiscal deficit is running at 6-7% of GDP – levels that are unlikely to shrink. Doubts about the dollar’s credibility persist, and emerging-market central banks, led by China, continue to buy. China holds only about a tenth of its reserves in gold, compared with roughly half in developed economies, leaving substantial room for further purchases.

Positioning

We recognize that AI now dominates both markets and the economy, and that the bull market depends on its continued success. It also depends on the Fed not cutting the cycle short by becoming too restrictive.

Overall, we remain constructive while staying prepared for volatility. In our framework, a moderate summer correction would be a healthy development within an ongoing bull market, as long as the key drivers – earnings growth and the AI productivity engine – remain intact and a later shift toward easier policy continues to look plausible.

After a strong first half, we have therefore taken some profits in equities while staying overweight. We would not be surprised to see the market rotate out of the momentum cohort toward broader participation. That could feel painful for some, but it would leave the market on a firmer footing for a fourth-quarter rally.

In addition to trimming gold, we sold our remaining commodity exposure in early June. We are using part of the proceeds to add corporate bonds and keeping the rest in liquidity, ready to redeploy on weakness.

Sources: Bloomberg and Bloomberg Intelligence, J.P. Morgan (Michael Cembalest), Morgan Stanley (Mike Wilson), Citadel Securities (Scott Rubner), Schroders (Jim Luke), Goldman Sachs, Strategas, Citrini Research, Bank of England, Financial Times, and other research partners.

-

Shock, Resilience, and Resolution: Na...Market View April

-

Geopolitics Increase Volatility – Fun...Market View March

-

Markets, Volatility & Productivit...Market View February

-

Goldilocks First, Overheating Later —...Market View January

-

Dovish Fed Pivot, Labor Softening &am...Market View December

-

The AI Supercycle, Fed Easing & a...Market View November

-

Skepticism Fuels the Bull: Under-Owne...Market View October

-

AI Momentum, Fed Shift, Inflation WatchMarket View September

-

Rally Faces Headwinds: Markets Remain...Market View August

-

The return of Goldilocks is taking shapeMarket View July

-

Resilient stock markets have more roo...Market View June

-

Markets Recover Despite Fragile Senti...Market View May

-

US Tariffs and Their Impact: Risks fo...Market View April

-

Market Upheaval: US Protectionism and...Market View March

-

Markets on the move: Volatility, AI c...Market View February

-

After the Rally: Market Volatility an...Market View January

-

Positive momentum and US exceptionali...Market View December

-

Resilient US growth amid election unc...Market View November

Disclaimer

This Publication was created with the assistance of artificial intelligence on 02.07.2026 02.07.2026.

The information contained in this document constitutes a marketing communication from FINAD (FINAD AG, Zurich; FINAD GmbH, Vienna or FINAD GmbH, Hamburg branch). This marketing communication has not been prepared in accordance with legislation promoting the independence of investment research and is not subject to any prohibition on trading following the dissemination of investment research. This document is for general information purposes only and for the personal use of the recipient of this document (hereafter referred to as “recipient”). It does not constitute a binding offer or invitation by or on behalf of FINAD to purchase, subscribe, sell or return any investment or to invest in any particular trading strategy or to engage in any other transaction in any jurisdiction. It does not constitute a recommendation by FINAD in legal, accounting or tax matters or a representation by FINAD as to the suitability or appropriateness of any particular investment strategy, transaction or investment for any individual recipient. A reference to past performance should not be construed as an indication of the future. The information and analyses contained in this publication have been compiled from sources believed to be reliable and credible. However, FINAD makes no warranty as to their reliability or completeness and disclaims any liability for losses arising from the use of this information. All opinions and views represent estimations that were valid at the time of going to press; we reserve the right to make changes at any time without obligation to update or communicate them. Before making any investment, transaction or other financial decision, recipients should clarify the suitability of such investment, transaction or other business for their particular circumstances and independently (with their professional advisors if necessary) consider the specific risks and the legal, regulatory, credit, tax and accounting consequences. It is the responsibility of the respective recipient to verify that he/she is entitled under the law applicable in his/her country of residence and/or nationality to request, receive and use this publication for personal purposes. FINAD declines any liability in this respect. An investment in the funds and other financial instruments mentioned in this document should only be made after careful reading and examination of the latest sales prospectus, the fund regulations and the legal information contained therein and after prior consultation with your client advisor and – if necessary – your own legal and/or tax advisor. It is the responsibility of the respective recipient to check whether he is entitled to request and receive the relevant fund documents under the law applicable in his country of residence and/or nationality. Neither this document nor copies thereof may be sent to or taken into the United States or distributed in the United States or handed over to US persons.

This document may not be reproduced in part or in full without the prior written consent of FINAD.

For Switzerland: FINAD AG, Talstrasse 58, 8001 Zurich, Switzerland is a public limited company specialized in financial services and asset management, established under Swiss law. FINAD is authorised as asset manager by the Swiss Financial Market Supervisory Authority (FINMA) and supervised by the Supervisory Organization (SO) AOOS. FINAD is also associated with OFS Ombud Finance Switzerland (http://www.ombudfinance.ch). Complaints about FINAD can be addressed to SO AOOS or OFS.

For Austria: FINAD GmbH, Dorotheergasse 6-8/L021, 1010 Vienna, Austria is an investment firm according to Section 3 of the Austrian Securities Supervision Act 2018 (WAG 2018) and as such is entitled to provide investment services of investment advice, portfolio management as well as the acceptance and transmission of orders, in each case with regard to financial instruments. FINAD is not authorized to provide services that involve holding clients’ money, securities or other instruments. FINAD is subject to the supervision of the Financial Market Authority (FMA), Otto-Wagner-Platz 5, 1090 Vienna (www.fma.gv.at). Complaints about FINAD may be submitted to the FMA.

For Germany: FINAD GmbH Deutschland, Schauenburgerstraße 61, 20095 Hamburg, Germany is the German branch of FINAD GmbH, Dorotheergasse 6-8/L/021, AT-1010 Vienna, Austria. FINAD is an independent securities services company specialized in investment advice, investment brokerage and asset management (financial portfolio management). The provision of securities services by FINAD is subject to the supervision of the Financial Market Authority (FMA), Otto-Wagner-Platz 5, 1090 Vienna, Austria (www.fma.gv.at) as well as the Federal Financial Supervisory Authority (BaFin), Graurheindorfer Straße 108, 53117 Bonn, Germany and Marie-Curie-Straße 24-28, 60439 Frankfurt am Main, Germany (www.bafin.de). Complaints about FINAD can be addressed to the FMA or BaFin.

FINAD is not authorized to practice law, provide tax advice or auditing services.

© Copyright FINAD – all rights reserved.

For more details about the company, please visit https://finad.com/en/imprint.