Market View December

Dovish Fed Pivot, Labor Softening & Buybacks Fuel the Year-End Bid

created by Ullrich Fischer, Chief Investment Officer

-

Shock, Resilience, and Resolution: Na...

-

Geopolitics Increase Volatility – Fun...Market View March 2026

-

Markets, Volatility & Productivit...Market View February 2026

-

Goldilocks First, Overheating Later —...Market View January 2026

-

The AI Supercycle, Fed Easing & a...Market View November 2025

-

Skepticism Fuels the Bull: Under-Owne...Market View October 2025

-

AI Momentum, Fed Shift, Inflation WatchMarket View September 2025

-

Rally Faces Headwinds: Markets Remain...Market View August 2025

-

The return of Goldilocks is taking shapeMarket View July 2025

-

Resilient stock markets have more roo...Market View June 2025

-

Markets Recover Despite Fragile Senti...Market View May 2025

-

US Tariffs and Their Impact: Risks fo...Market View April 2025

-

Market Upheaval: US Protectionism and...Market View March 2025

-

Markets on the move: Volatility, AI c...Market View February 2025

-

After the Rally: Market Volatility an...Market View January 2025

-

Positive momentum and US exceptionali...Market View December 2024

-

Resilient US growth amid election unc...Market View November 2024

Executive Summary

Macro backdrop: The hawkish tone from the Fed’s October meeting and subsequent FOMC member commentary triggered a liquidity-driven market selloff. However, last week, key FOMC voting members — Governor Waller and New York Fed President Williams — signaled support for a December rate cut. This shift in tone reversed market expectations and sparked an equity rebound. We see increasing signs that the market has now found its bottom.

Markets: Beneath the surface, market damage was significantly deeper than a 5% drop on headline indices suggested: the median S&P 500 stock declined roughly 16%, highlighting the market’s narrow leadership and pronounced weakness in lower-quality, liquidity-sensitive names. This correction served to reset stretched positioning, technicals, and sentiment.

Monetary policy: In our view, the Fed has shifted back to a dovish posture, focusing on labor market weakness and strains in money-market liquidity. Kevin Hassett seems to be the frontrunner to replace Powell. Such a nomination would carry fresh risks but would likely add fuel to the debasement trade in 2026.

Outlook: We think depressed sentiment and an upcoming wave of corporate buybacks create a favorable setup for a December rally amid a strong seasonal period. We used the recent weakness to add to our overweight position, and we remain constructive on the medium-term outlook. History suggests that bull markets rarely end during cutting cycles. We see no structural evidence to argue this time is different.

Monthly Review

- The S&P 500 entered its first 5% correction since April. So far, there have been eight S&P 500 corrections of 5% or more during this bull market that began in 2022. Only the “Liberation Day” correction was meaningfully deeper than 10%.

- The sharp rebound late last week was sparked by New York Fed President John Williams, who signaled a strong inclination to cut rates, stating that labor-market weakness poses a greater risk than inflation.

- As head of the New York Fed, Williams oversees the Fed’s balance sheet and money-market operations. His comments carry particular weight, especially given his prior view that the Fed may soon need to expand its balance sheet again amid rising interbank market stress.

- Williams is also a close ally of Chair Powell, suggesting the Chair is likewise inclined to support a December cut. Market-implied odds of a rate cut jumped from as low as 25% to around 80% following Williams’ dovish remarks, indicating markets now see a highly probable December move.

- The correction reset key technical and sentiment indicators. For example, on Friday, 21 Nov 2025, over USD 1 billion traded in the 3x inverse S&P 500 ETF (SPXU). Historically, similar volume spikes in this vehicle have coincided with major market lows, including the COVID trough, the 2022 bear-market lows, and the April 2025 “Liberation Day” bottom.

- Twelve of this year’s fifteen best-performing markets are emerging markets, recently led by LatAm, according to Ned Davis Research. Relative flows into EM ETFs are trending higher while US flows trend lower, potentially reflecting a shift toward more attractive valuations.

Market Development – Labor market slack justifies further Fed rate cuts

World

While September US payrolls were better than expected—albeit already dated—and initially pointed to stable labor demand, the concurrent rise in the unemployment rate signals emerging slack.

- The unemployment rate has risen to 4.4%, the highest since October 2021.

- After revisions, two months this year (June and August) now show negative payrolls.

- This labor-market softening is important. It should help contain inflation and provide strong justification for the Fed to continue its rate-cutting cycle.

- A key downside growth risk remains persistently weak US consumer sentiment, which could weigh on critical holiday spending.

Inflation Outlook: Based on the September CPI and PPI data, Core PCE (core inflation) appears to be tracking near 2.8%, which supports the Fed’s move toward a more dovish stance.

Global PMIs: The November flash PMIs show major economies expanding, led primarily by services, suggesting underlying business resilience.

Japan: Q3 GDP contracted –0.4% from Q2, reflecting trade frictions and domestic consumption pressures. The weakness argues for additional fiscal support and further delays to any Bank of Japan policy normalization, keeping settings loose.

China: A new structural driver is the government-mandated push for AI integration. The State Council has launched an extensive initiative to embed generative AI across manufacturing, healthcare, and public administration, with targets including >90% penetration of intelligent terminals and AI agents by 2030.

Europe

- Official data confirm that Europe’s economy is effectively stagnating: Euro Area growth is just above 1%, Germany is flat, manufacturing is weak, and domestic demand remains sluggish. Reflecting a larger structural drag from tougher Chinese export competition and lower potential growth, Goldman Sachs now forecasts Euro Area real GDP growth at 1.2% in 2026 and 1.3% in 2027 (down from 1.3% and 1.5%).

- Heading into winter, Europe’s gas (LNG) position looks more comfortable. LNG regasification capacity in the EU has increased by ~45% between Q3 2021 and Q3 2025, easing bottlenecks and improving market integration through more cross-border flows and greater price convergence. Current reports suggest ample spare terminal capacity and—given subdued Asian demand—plenty of LNG available for Europe. The region still receives Russian gas via TurkStream and as LNG, but this now amounts to only around a quarter of pre-war volumes.

Switzerland

- European earnings growth is currently split into three buckets: “rapid” growth, early re-acceleration, and flat. Spain (+21%), the Netherlands (+15%), and Switzerland (+12%) lead the rapid bucket. Spain and the Netherlands have topped S&P 500 earnings growth in recent years, and all three markets have outperformed US equities in USD terms this year—though Dutch figures are skewed by ASML.

- Swiss macro data continue to highlight the drag from tariffs, with October exports falling again, including a roughly 6% decline to the US. This weakness increases pressure on policymakers to curb further franc appreciation. While the latest trade agreement should reduce the tariff rate from 39% to 15%, that level remains elevated for a highly export-dependent economy—especially after two rounds of front-loading and already subdued growth.

A strong trade-weighted franc is also weighing on competitiveness: EUR/CHF has rebounded from ~0.92, and Swiss authorities are likely to defend this area while inflation remains below target, leaving the franc an unattractive safe haven.

Equity correction seen as froth cleansing for year-end rally

Current market conditions are highly sensitive to sentiment and liquidity, whipsawed by shifting Fed-cut expectations, the absence or staleness of US data (due to the government shutdown), AI-bubble fears, and crypto volatility. Underlying this is a weakening labor market amid stable inflation—developments that ultimately justify further rate cuts.

We view the recent sell-off as a technical, liquidity-driven correction—a momentum reset that is now closer to its end than its beginning. Our medium-term outlook remains constructive—we stay bullish.

The correction began in the lowest-quality, most liquidity-sensitive segments. Speculative high-flyers—meme stocks, unprofitable tech, SPACs, and crypto-sensitive names—all experienced abrupt sell-offs starting in late September as liquidity tightened.

While the S&P 500 only saw a modest decline, the damage beneath the surface was severe: two-thirds of the largest 1,000 stocks were down more than 10%, and a quarter were down more than 20%. To us, this deflation of froth is healthy and extends the longevity of the current bull-market cycle.

Flow-of-funds data confirm that this was a cleansing event, showing genuine capitulation from hedge funds, systematic strategies, and real-money investors. That said, we expect structurally higher realized volatility to remain a feature through 2026, but within an ongoing bull regime.

The Fed and labor data are central to this story. Private-sector indicators already point to sufficient labor-market weakness, in our view, to warrant a continued rate-cutting cycle. However, with the official government labor data—on which the Fed formally relies—unavailable due to the shutdown, policy visibility is impaired. October’s jobs report was canceled, and November’s release has been postponed to 16 December, after the 10 December FOMC meeting. As a result, markets are now forced to price in the risk of a Fed that is “behind the curve,” slow to recognize the extent of labor-market deterioration. This tension between what alternative data imply and what the Fed is willing to concede has been a major driver of the current correction.

The December FOMC meeting is therefore crucial for markets. Our base case—following the dovish comments from NY Fed President Williams last Friday—is a rate cut. However, this is unlikely to be a straightforward meeting. The FOMC is as divided as it has been in decades; currently, it appears there is a 7–5 majority for a December rate cut. The last 7–5 split occurred in 1983. There is even a non-trivial risk that a key member flips to vote for no change, potentially resulting in a 6–6 tie—an outcome the Fed has never faced.

With no explicit tie-break mechanism in the Federal Reserve Act, a tie would typically leave the funds rate unchanged until the committee either revotes during the same meeting or revisits the decision later. For markets, these institutional nuances will matter much more going forward given the political pressure on the Fed.

Beyond December, Fed leadership becomes a key factor. An announcement on the new Fed Chair is expected before Christmas, ahead of the formal transition in May 2026.

Our preferred candidates are Rick Rieder or Chris Waller—both dovish and highly credible in the eyes of the market. Betting markets, however, currently see Kevin Hassett as the frontrunner, with odds recently exceeding 50%. A Hassett-led Fed would be ultra-dovish and strongly aligned with Trump.

The key risk is that an overly accommodative Fed stance could erode market confidence and lead to a sharp rise in inflation expectations in 2026. In such a scenario, the debasement trade and bubble risks could accelerate rapidly, while the USD weakens further and the yield curve steepens.

The constructive scenario for a Hassett-led Fed is one in which both Trump and Hassett rely heavily on Treasury Secretary Bessent—effectively allowing him to coordinate fiscal and monetary policy behind the scenes to maintain market confidence. In our view, Bessent understands that the Fed Chair must demonstrate independence to earn the trust of colleagues and markets. It is also not guaranteed that the Senate would confirm Hassett.

From a liquidity standpoint, the outlook into year-end and early 2026 is improving:

1. A December rate cut is now widely expected.

2. The Treasury General Account is likely to decline as the government fully reopens, releasing reserves into the banking system.

3. The Fed will wind down quantitative tightening (QT) effective December 1st.

These actions are urgently needed. If the Fed delivers this liquidity easing, the biggest beneficiaries should once again be the usual suspects: the Nasdaq 100, gold and crypto. We believe the Fed has learned from past mistakes (e.g., Q4 2018) and will act meaningfully this time.

Positioning

History suggests that bull markets rarely end during cutting cycles, and we see no evidence indicating that this time will be different. To us, this is a technical, liquidity-driven correction within an ongoing bull market. The severe damage in weaker segments, investor capitulation, and an improving liquidity impulse all suggest that we are nearing the end of this reset. Furthermore, the core earnings cycle remains strong, supported by aggressive, growth-driving investments in AI infrastructure.

Hence, we used the market weakness to further increase our equity overweight in selected quality stocks and emerging markets.

Technical Picture: The S&P 500 has rebounded cleanly from key support at the 100-day moving average near 6,500–6,550. The bounce is solid, but with no decisive trend since September, the market still looks range-bound, suggesting more sideways volatility is certainly possible before any decisive breakout and a potential year-end rally.

Leadership Trends: Market leadership during the sell-off was not overly defensive, mirroring patterns that are consistent with smaller historical corrections.

Mega-Cap Resilience: The Magnificent 7 have traded in line with the historical average drawdown. More telling, earnings estimates have been revised higher for the cohort and for growth sectors overall. That backdrop argues this is a routine correction rather than the onset of a sustained bear market.

Buybacks: Corporate buybacks have been a consistent pillar of support this year. At the depths of “Liberation Day,” corporate demand made up more than 8% of daily trading, helping to establish the bottom. Historically, when buybacks exceed ~1% of daily volume, returns tend to run at roughly twice the daily average. With activity still robust, 3Fourteen Research expects buybacks to remain above 1% of volume through most of December, aided by typical year-end seasonality.

Bitcoin: Bitcoin fell nearly 30% in 30 days. Its Sharpe ratio has collapsed to zero, a level that has historically preceded major reversals (2019, 2020, 2022). However, historical precedent suggests potential weakness for another 30–40 days before a sustainable uptrend can emerge.

Yields: Our expected 10-year US yields range for 2026 is 3.25%–4.5%, with a tendency toward higher yields in the first half of 2026 if Hassett is announced as the new Fed Chair.

Gold: We maintain our overweight position. Strong investment demand and ongoing central bank purchases are driving a physical market deficit in 2025, with mine-supply remaining flat, according to Vontobel. Speculative excess has been washed out. The secular bull market remains intact.

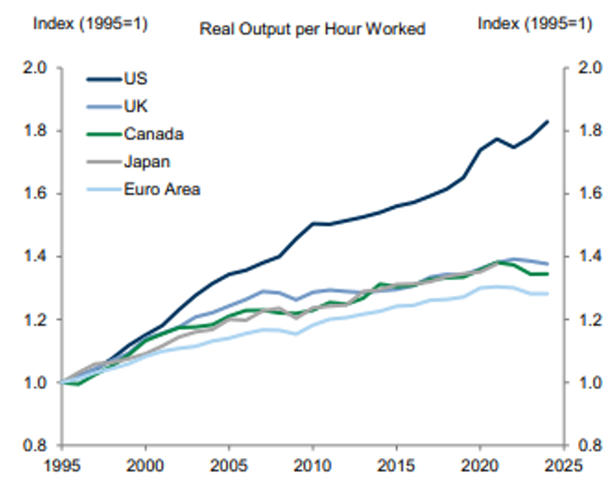

US Productivity Outperformance

Source: Goldman Sachs

Since 1995 — according to Goldman Sachs — US labor productivity has grown at an average annual rate of 2.1%, more than twice the pace of other advanced economies. Of this gap, around 0.55 percentage points reflect faster growth in capital inputs (i.e., higher investment), about 0.35 percentage points stem from stronger total factor productivity growth, and the remainder is driven by shifts in labor-force characteristics (such as higher education levels). Looking ahead, the structural forces behind this three-decade divergence, reinforced by strong tailwinds from AI adoption, are likely to keep US productivity outperforming that of other advanced economies.

Sources: Bloomberg, Morgan Stanley, Bank of America, Goldman Sachs, The Macro Compass, The Market Ear, Steno Research, 42Macro, JPM, Hightower Naples, Strategas, FT, BCA Research, Renaissance Macro, BlackRock, 3Fourteen Research, TS Lombard, Ned Davis Research, Vontobel

-

Shock, Resilience, and Resolution: Na...

-

Geopolitics Increase Volatility – Fun...Market View March

-

Markets, Volatility & Productivit...Market View February

-

Goldilocks First, Overheating Later —...Market View January

-

The AI Supercycle, Fed Easing & a...Market View November

-

Skepticism Fuels the Bull: Under-Owne...Market View October

-

AI Momentum, Fed Shift, Inflation WatchMarket View September

-

Rally Faces Headwinds: Markets Remain...Market View August

-

The return of Goldilocks is taking shapeMarket View July

-

Resilient stock markets have more roo...Market View June

-

Markets Recover Despite Fragile Senti...Market View May

-

US Tariffs and Their Impact: Risks fo...Market View April

-

Market Upheaval: US Protectionism and...Market View March

-

Markets on the move: Volatility, AI c...Market View February

-

After the Rally: Market Volatility an...Market View January

-

Positive momentum and US exceptionali...Market View December

-

Resilient US growth amid election unc...Market View November

Disclaimer

This Publication was created on 27.11.2025.

The information contained in this document constitutes a marketing communication from FINAD (FINAD AG, Zurich; FINAD GmbH, Vienna or FINAD GmbH, Hamburg branch). This marketing communication has not been prepared in accordance with legislation promoting the independence of investment research and is not subject to any prohibition on trading following the dissemination of investment research. This document is for general information purposes only and for the personal use of the recipient of this document (hereafter referred to as “recipient”). It does not constitute a binding offer or invitation by or on behalf of FINAD to purchase, subscribe, sell or return any investment or to invest in any particular trading strategy or to engage in any other transaction in any jurisdiction. It does not constitute a recommendation by FINAD in legal, accounting or tax matters or a representation by FINAD as to the suitability or appropriateness of any particular investment strategy, transaction or investment for any individual recipient. A reference to past performance should not be construed as an indication of the future. The information and analyses contained in this publication have been compiled from sources believed to be reliable and credible. However, FINAD makes no warranty as to their reliability or completeness and disclaims any liability for losses arising from the use of this information. All opinions and views represent estimations that were valid at the time of going to press; we reserve the right to make changes at any time without obligation to update or communicate them. Before making any investment, transaction or other financial decision, recipients should clarify the suitability of such investment, transaction or other business for their particular circumstances and independently (with their professional advisors if necessary) consider the specific risks and the legal, regulatory, credit, tax and accounting consequences. It is the responsibility of the respective recipient to verify that he/she is entitled under the law applicable in his/her country of residence and/or nationality to request, receive and use this publication for personal purposes. FINAD declines any liability in this respect. An investment in the funds and other financial instruments mentioned in this document should only be made after careful reading and examination of the latest sales prospectus, the fund regulations and the legal information contained therein and after prior consultation with your client advisor and – if necessary – your own legal and/or tax advisor. It is the responsibility of the respective recipient to check whether he is entitled to request and receive the relevant fund documents under the law applicable in his country of residence and/or nationality. Neither this document nor copies thereof may be sent to or taken into the United States or distributed in the United States or handed over to US persons.

This document may not be reproduced in part or in full without the prior written consent of FINAD.

For Switzerland: FINAD AG, Talstrasse 58, 8001 Zurich, Switzerland is a public limited company specialized in financial services and asset management, established under Swiss law. FINAD is authorised as asset manager by the Swiss Financial Market Supervisory Authority (FINMA) and supervised by the Supervisory Organization (SO) AOOS. FINAD is also associated with OFS Ombud Finance Switzerland (http://www.ombudfinance.ch). Complaints about FINAD can be addressed to SO AOOS or OFS.

For Austria: FINAD GmbH, Dorotheergasse 6-8/L021, 1010 Vienna, Austria is an investment firm according to Section 3 of the Austrian Securities Supervision Act 2018 (WAG 2018) and as such is entitled to provide investment services of investment advice, portfolio management as well as the acceptance and transmission of orders, in each case with regard to financial instruments. FINAD is not authorized to provide services that involve holding clients’ money, securities or other instruments. FINAD is subject to the supervision of the Financial Market Authority (FMA), Otto-Wagner-Platz 5, 1090 Vienna (www.fma.gv.at). Complaints about FINAD may be submitted to the FMA.

For Germany: FINAD GmbH Deutschland, Schauenburgerstraße 61, 20095 Hamburg, Germany is the German branch of FINAD GmbH, Dorotheergasse 6-8/L/021, AT-1010 Vienna, Austria. FINAD is an independent securities services company specialized in investment advice, investment brokerage and asset management (financial portfolio management). The provision of securities services by FINAD is subject to the supervision of the Financial Market Authority (FMA), Otto-Wagner-Platz 5, 1090 Vienna, Austria (www.fma.gv.at) as well as the Federal Financial Supervisory Authority (BaFin), Graurheindorfer Straße 108, 53117 Bonn, Germany and Marie-Curie-Straße 24-28, 60439 Frankfurt am Main, Germany (www.bafin.de). Complaints about FINAD can be addressed to the FMA or BaFin.

FINAD is not authorized to practice law, provide tax advice or auditing services.

© Copyright FINAD – all rights reserved.

For more details about the company, please visit https://finad.com/en/imprint.